Some of its firms are old colleagues who acted together in the middle of Detroit’s bankruptcy. The economic crisis, the fiscal debacle and the junk bonds were the bait that attracted them to Puerto Rico in 2014. Now, in the midst of the humanitarian crisis that the country is experiencing over the destruction of Hurricane Maria, the Ad Hoc Group of General Obligation Bonds rejects that all federal funds allocated to the island after the catastrophe can not be touched by the bondholders.

The initial order to protect federal funds from bondholders was filed by the Puerto Rican government and the Fiscal Control Board (JCF) before federal Judge Laura Taylor Swain, in the bankruptcy case under Title III of the PROMESA Act.

“Federal reimbursement funds,” with which the government replaces its expenses in the emergency, “should not be excluded from creditors’ claims, liens, or priorities, because they merely replace funds previously spent by the Commonwealth from its own resources for the purposes designated in the federal program,” says the Ad Hoc Group objection.

Several Title III creditors, including insurers, have also raised limited objections to the government’s stance. The Center for Investigative Journalism (CPI in spanish) consulted with a a few sources who analyzed the Ad Hoc motion and they agreed that the group makes a distinction between funds from FEMA and other federal agencies such as the Department of Housing and Urban Development, the Department of Health and Human Resources or the Small Business Administration, and the federal statutes authorizing the various grants. For this reason, they want the government of Puerto Rico to be more precise as to the origin of the funds expected to arrive and on what legal basis they are considering granting them. This is perhaps an attempt to prevent the Puerto Rican government from having carte blanche in the use of the funds and creating the perception that the billions of dollars allegedly coming to the island all come from disaster relief funds.

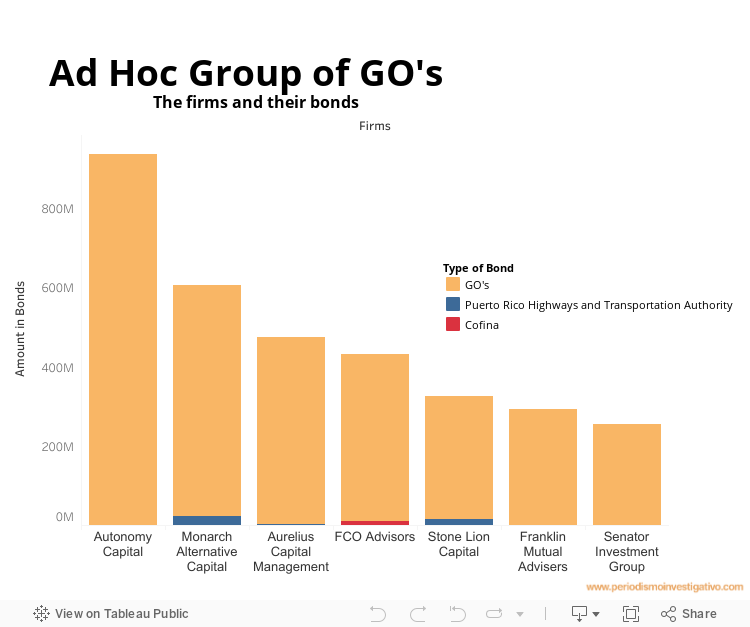

The group of creditors consists of the vulture funds Aurelius Capital, Autonomy Capital, Fundamental Advisors, Monarch Alternative, Senator Investment, Stone Lion Capital; and the mutual fund Franklin Mutual Advisers. In total they claim $3.3 billion in General Obligation bonds. They also have bonds from the Corporation for the Appealing Interest Fund (known as COFINA) and the Highway and Transportation Authority (HTA).

In Detroit, Aurelius Capital Management, Stone Lion Capital and Monarch Alternative Capital, were opposed until the last moment to a plan of “friendly” restructuring in search of the collection of bonds that bought at a discount. And now, the government of Puerto Rico’s bankruptcy case is the scenario for the reunion of these players with experience litigating in debt collections from countries, cities or companies that are in the financial abyss.

In the Ad Hoc Group, Autonomy Capital is claiming the largest amount: more than $900 million in General Obligation bonds. It is an affiliate of Autonomy Americas, incorporated in the tax haven of the Channel Islands, an archipelago near France. It has more than $4 billion in funds under management and its clients are insurance companies, foundations, public and private pension systems, and high net worth individuals, accredited as specialized investors. The minimum amount required to invest in Autonomy funds is between $5 million and $10 million.

Robert Gibbins, former partner of the defunct Lehman Brothers, and Derek Goodman, who worked for UBS/Swiss Bank, are the chief executives of Autonomy, based in New York and with offices in Madrid, London, Switzerland and Sao Paulo. The firm invests primarily in companies that trade on the stock exchange. They also run the Autonomy Venezuela Opportunities Fund, which focuses on securities of that country. In August 2017, Autonomy acquired more than half of the shares of Adecoagro, Argentina’s agricultural products company with productive lands and industrial plants in Argentina, Uruguay and Brazil.

Meanwhile, Monarch Alternative Capital, prefers to bet on carbon. They own $190 million (11%) of Arch Coal, the second U.S. company to supply that mineral to power generators. In the Ad Hoc Group, they are the second firm to claim the largest amount of debt: more than $500 million in General Obligation bonds, and more than $21 million in HTA bonds.

Monarch Alternative has on its work team former executives from other vulture funds that have Puerto Rican bonds, such as Stone Lion Capital, Golden Tree Asset Management, Davidson Kempner and Och-Ziff Capital. There are also former executives from JP Morgan and Rothschild & Co.

Founded in 2002 by Michael Weinstock, Andrew Herenstein and Chris Santana, former bankers at Lazard Frères & Co., as of June 30, 2017, Monarch managed approximately $4.6 billion and had 63 employees, including 20 investment managers in offices in New York and London.

In 2015, Monarch bought $23 million (according to the actual change in English Pound) in Four Seasons Health Care properties, the largest nursing home operator in Great Britain, which was carrying significant debt. In 2006, they bought Oneida Limited, one of the world’s largest designers and sellers of stainless steel items, after that company went into Chapter 11 bankruptcy.

The strategies of the GO Ad Hoc Group firms are those that distinguish vulture funds from hedge funds and other investment firms: their modus operandi consists of buying debt that is about to enter into default, or is already in that status, at a discount. In the case of public debt, they litigate against the country in the jurisdiction where the debt was issued, demanding payment of the original price.

“In the litigation, (vulture funds) demand full payment of principal, plus regular interest, which may have included compensation for default risk, and ‘compensatory’ interest for non-payment under the contract’s original terms, which in practice are punitive,” said Economist Martín Guzmán, a researcher at Columbia University, New York, and a professor at the University of Buenos Aires, Argentina.

Aurelius, Stone Lion, Monarch, Fundamental Advisors and Franklin Advisers bought part of the 2014 General Obligation bond issue, rated as high risk by the main credit agencies.

Fundamental Advisors has an uncomfortable position because it owns General Obligation bonds (more than $400 million) in addition to Cofina Subordinate bonds (more than $10 million.) As part of the Ad Hoc Group, the firm would be taking positions against its own Cofina bond investments. Hector Negroni, chief investment officer of Fundamental Credit Opportunities (FCO), a division of Fundamental Advisors that owns the bonds of Puerto Rico, did not respond to an interview request from the CPI.

In October 2016, five funds called Jacana Holdings belonging to FCO participated in a lawsuit with other firms from the Ad Hoc Group asking the government to stop using the portion of the Sales and Use Taxes (IVU) that previously went to pay Cofina bonds to pay General Obligation bond debt, because this debt has constitutional payment priority. The same argument has been used by the Ad Hoc Group’s defense in Title III, for one of the central disputes of the case.

Franklin Mutual Advisers is in a similar position to FCO’s, since they claim the collection of General Obligation bonds as part of the Ad Hoc Group, while another 22 funds owned by its same parent company, Franklin Templeton, are demanding the payment of Cofina bonds from within the Mutual Fund Group.

Within the group dominated by vulture funds, Franklin Advisers is the only mutual fund. Mutual funds and vulture funds have different legal structures and regulations and use different investment strategies. While the vultures, officially registered as hedge funds, invest to recover short-term gains and manage money from specialized investors, usually from $1 million and up, mutual funds invest to recover in the long run, and the money they commonly handle is from non-specialized individuals and entities.

But by acting in conjunction with vulture funds, mutual funds and other investment firms can follow their strategies.

“Given the expectation of such high returns associated with these kinds of strategies, other bondholders are encouraged to pursue similar behavior, or simply to follow the leadership of a vulture fund, refusing to be part of the restructuring, waiting for the favorable decision for the vulture fund, and then calling for a similar treatment, as in many cases in Argentina’s dispute in the U.S. court,” said Economist Martín Guzmán in “Restructuring sovereign debt in a financial-legal structure with gaps” published in the University of Puerto Rico’s “Law Review.”

In trying to have greater influence in the Title III case, the Ad Hoc Group tried to have two of its members appointed to the Unsecured Creditors Committee, comprised mainly of government providers.

It is very common for vulture fund executives to be former bankruptcy lawyers, as is the case with the tight-lipped Mark Brodsky, founder and manager of Aurelius Capital, who for 16 years worked in major law firms in New York. Much of that time, in the early 1990s, he served as an attorney and co-head of the bankruptcy practice at Kramer, Levin, Naftalis & Frankel (Title III present mutual fund attorneys.) From 1996 to 2005, Brodsky was a partner in Elliott Management Corporation, a vulture fund owned by financial tycoon Paul Singer, who fought alongside Aurelius and other firms for the collection of Argentine debt.

Brodsky founded Aurelius in 2006 with $325 million in capital, of which more than half came from pension funds and foundations. Aurelius Capital has $3.5 billion in funds under management and focuses on investing in high-risk debt.

Aurelius tried to “wriggle out” of losses on its AIB bonds by engaging “powerful lobbyists” to get the US Treasury, the State Department and members of Congress to apply pressure on Ireland. In Greece, in 2012, in the midst of the European country’s financial turmoil, the government had to face what was described as a “small well-funded group of investors” who opposed a 75% haircut. Aurelius Capital was in that group. In the UK, in 2013, they opposed a $500 million cut in Co-operative Bank debt, they won, and took control of the bank’s 10% stake. In Brazil’s Petrobras, they forced a $54 billion default as a “precautionary measure.” They also attempted to upset a Tribune Co. bankruptcy plan that had been approved by most creditors; but in that attempt, they failed.

In Puerto Rico government’s bankruptcy case, Aurelius claims more than $470 million in General Obligation bonds, and more than $2 million in HTA bonds.

Firms expose themselves to the press

The room is filled with more than 20 Puerto Rican and U.S. mainland journalists who came to speak with the executives of various hedge funds convened by the Ravitch Fiscal Reporting Program of the City University of New York (CUNY.) It’s strange, because hedge funds barely answer calls from the press.

Eric Michael Friel, senior managing director of Stone Lion Capital, a hedge fund member of the Ad Hoc Group, said “Contrary to popular belief, I believe investors and hedge funds want many of the same things that the people of Puerto Rico do.” Among the things they want, he mentioned parity in Medicaid funding and better education.

However, the Ad Hoc Group of General Obligation bonds launched its offensive against the government of Puerto Rico in 2015, when they commissioned a report to show that the government could repay its debts. The report, titled “For Puerto Rico, There is a Better Way,” recommends the dismissal of teachers, cuts in the subsidy granted to the University of Puerto Rico and in “excess Medicaid benefits,” among other austerity measures.

Friel, a former CEO and “risky debt” analyst at Bear Stearns & Co., one of the first banks to collapse in the 2008 financial crisis, said his father was a teacher. “I understand the value of a good education, that is the last thing I want taken away from the people of Puerto Rico,” he said.

Centro de Periodismo Investigativo

Eric Michael Friel at City University of New York

The Center for Investigative Journalism asked Friel: At what price did Stone Lion Capital buy the bonds from the 2014 General Obligation issue and how much do you expect to receive in return? “I do not know the answer, I think it is wrong to focus on that, knowing that is not going to solve Puerto Rico’s problems, it literally will not help anyone with anything,” he said after having demanded transparency from the Fiscal Control Board and the government of Puerto Rico during his meeting with the press.

Stone Lion Capital was founded by Alan Jay Mintz and Gregory Augustine Hanley, who like Friel, were former risky debt dealers at Bear Stearns, the bank that infected the financial market with toxic mortgage assets, received a bailout from the Federal Reserve Bank and was later sold to JP Morgan.

Without wasting any time, in 2008 the two former Bearn Stearns partners founded Stone Lion Capital in New York. In 2014, they requested $100 million from the Puerto Rico government’s junk bond issue, from which they had $30 million allocated. But Stone Lion has more General Obligation bonds: In the bankruptcy proceedings they claim more than $300 million in such bonds that they could have obtained before or after the 2014 issue. They also have more than $15 million in bonds from the HTA.

Among those who attended during the session for journalists at CUNY was Julio Cabral-Corrada, a Puerto Rican partner at Stone Lion Capital. Corrada joined this hedge fund immediately after leaving his position at Morgan Stanley in November 2014, just nine months after that bank served as a seller of the General Obligation bond issue of which Stone Lion bought $30 million. Morgan Stanley is under federal investigation for that transaction. In 2014, Cabral-Corrada organized a fundraising activity for Puerto Rico’s former Resident Commissioner in Washington, Pedro Pierluisi.

Also attending that unusual meeting between investors and journalists was Héctor Negroni, chief executive of FCO.

Centro de Periodismo Investigativo

Héctor Negroni at City University of New York

“I am from a Puerto Rican family, my family is from the island and I have been an investor in the municipal market for 30 years. For me, this is a deeply intense and personal battle,” Negroni said in English, referring to the Puerto Rican government’s bankruptcy case.

Negroni wore a vest with the FCO logo on top of his checkered shirt. Sitting in a back row of the room, he listened to the other lecturers, and when he did not agree, he raised his voice to speak sharply over the speaker.

Negroni went on to lead FCO in 2012, after working as director of the municipal bond trading division at Goldman Sachs. He also worked for Lazard Freres Bank and Citibank. His political donations have focused on Republican candidates, including Senate Finance Committee Chairman Orrin Hatch, Charles Grassley, also a member of that committee, and the Goldman Sachs Group Political Action Committee, one of the major contributors to presidential campaigns of the Republican and Democrat parties. In 2007, he made a $1,000 donation to Puerto Rico’s former Resident Commissioner in Washington, Pedro Pierluisi.

“In fact, for a senior creditor, the GO, the ELA is completely solvent, it has no reason to be on default, there has no reason to be available bankruptcy”, Negroni said at the CUNY panel.

Senator Investment, another vulture fund in the group, was incorporated in 2008 in Delaware as a limited liability company with several funds in the Cayman Islands. Alexander Klabin, one of the founders, previously worked for Goldman Sachs, Monarch Alternative Capital and York Capital Management. His partner Douglas Silverman also left York Capital and previously worked for Merrill Lynch.

Its investments are diverse, including $1.65 million in the producer and seller of the Corona and Modelo beer brands, Constellation Brands, a company that is among the U.S. Fortune 500 companies, and in health insurance companies such as Humana, in which they had $224 million in shares until september 2017. It also owns $49 million in shares of Caesars Entertainment, a Las Vegas-based company that manages hotels and casinos. By September 2016, it had more than $13 billion in assets under management. In the case of the government of Puerto Rico’s bankruptcy, they claim $254,740,000 in General Obligation bonds.

And, in honor of its own name, Senator Investment has paid out $55,800 in political donations, many to Senate Republican and Democrat candidates, as well as presidential and U.S. House of Representatives campaigns, since its inception in 2008.

Although most of the country does not have electricity, water or access to communications after Maria’s hit, the general view of Title III will be resumed at 10am this Wednesday, October 25. This time it will not be in San Juan, but in the United States District Court for the Southern District of New York, Daniel Patrick Moynihan Courthouse, 500 Pearl Street, NY. It will be broadcast by videoconference in federal courtroom in San Juan.

The first item on the agenda is the FEMA-related motion filed by bondholders on how the funds will be managed for the country’s recovery, in light of the bankruptcy process. For tomorrow’s hearing, Ad Hoc Group executives, all with offices in New York, are walking distance.

Laura Moscoso collaborated on this story.

The “The creditors that control Puerto Rico’s bankruptcy” series of the Center for Investigative Journalism digs into in the characteristics and the background of the investment firms that until now have dominated the government of Puerto Rico’s bankruptcy case. The next stories will be published this and next week.

This reporting was supported by a grant from the Leonard C. Goodman Institute for Investigative Reporting.