SAN JUAN – Reverse mortgages are failing at nearly double the U.S. national average in Puerto Rico, a problem magnified on the island by sliding property values, lenders’ responses after natural disasters and unique challenges ranging from spotty mail service to the lack of some loan materials in Spanish.

Across the United States, the loans – which allow seniors to draw down equity in their homes – are falling into default at unprecedented rates a decade after the onset of the Great Recession, when brokers wrote the most loans in the program’s history.

An analysis by USA TODAY and the Centro de Periodismo Investigativo in Puerto Rico found waves of reverse mortgages headed to foreclosure for reasons other than death, the natural way the loans are supposed to end. Almost one in four reverse mortgage loans failed from 2014 to 2018 over technical snags, according to the Government Accountability Office.

Totals from 2019 compiled by the island’s office for financial institutions suggests an even greater share: 80% of the last year’s reverse mortgage foreclosures in 2019 were the result of tax defaults, insurance issues or occupancy problems.

Across the U.S., about one in seven loans met the same fate during those years, the USA TODAY analysis found. The work was done in partnership with Grand Valley State University in Michigan with support from the McGraw Center for Business Journalism and the Economic Hardship Reporting Project.

Each of the 1,617 foreclosures last year, and hundreds before them, represents a reverse mortgage loan that did not deliver on its original promise of stable housing as seniors age.

Nearly 70% of homes in Puerto Rico are occupied by their owners – far above the U.S. national average – creating a large potential market for reverse mortgages. In some parts of the island, including communities ringing San Juan, loan brokers wrote new loans at four times the rate of the entire U.S.

San Juan-based Moneyhouse dominated the reverse mortgage market there since 2007 and wrote nearly 4,300 of the island’s 10,800 loans through the end of last year. The company used a popular salsa singer for radio and television ads that entice seniors with the prospect of staving off monthly payments to better enjoy their retirement.

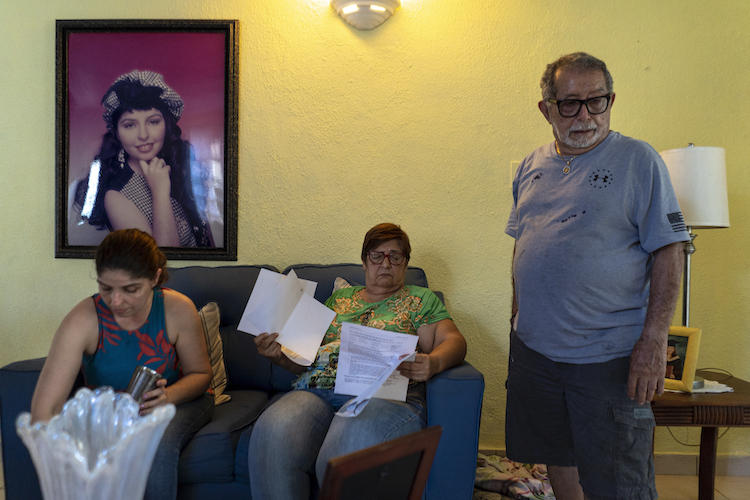

After seeing one of those TV spots featuring his favorite singer, José Sajiún Soto, 82, took out a reverse mortgage in 2013 for his home in San Juan’s Las Monjas neighborhood. Today, he regrets it, and he acknowledges he didn’t read all the fine print.

Moneyhouse has built years of local trust with customers, but, like other lenders, it sells its loans in the secondary market to U.S.-based servicers.

Photo by Cristina Martínez | Center for Investigative Journalism

Since 2007, the Moneyhouse has dominated the ‘reverse’ mortgage market in Puerto Rico.

Soto’s daughter, Ramona, says she routinely has to help her father deal with paperwork with the loan’s current Michigan-based servicer, Celink, that arrive in a jumble of English and Spanish threatening default for failure to pay homeowners insurance. Celink did not respond to a request for comment.

“They have said like 20 times that something was not paid and I would send them back evidence that it was paid and a copy of the check,” Ramona Soto said. “It is a problem that they don’t have an office here.”

Some loans issued by Moneyhouse to Puerto Rico residents included extra service charges significantly higher than in other parts of the country, too, according to an analysis of 2008 and 2009 federal loan data. Those fees were discontinued by the bank and others as lenders and servicers became more efficient, a bank spokesman said.

Company president and CEO David Levis defended the loans as “a godsend” for seniors who didn’t have enough Social Security or pension income to cover their bills.

But seniors on the island face unique challenges, said Tara Twomey, an attorney with the National Consumer Law Center who trains attorneys there on defending clients against foreclosure. A reverse mortgage failure can begin with something as basic as the island’s postal delivery, which in some areas relies on building names instead of traditional addresses.

“The system with reverse mortgages is not set up for success here,” Twomey said. “Seniors face compounding challenges, with a complicated product mixed with a language barrier, natural disaster and a lagging economy.”

Hurricane Maria: A tempest in reverse mortgages

Reverse mortgages require that borrowers must live in their home, keep the home maintained and stay current with taxes and hazard insurance – all things thrown into disarray by a hurricane.

Twomey said Puerto Rico seniors ran into trouble with the insurance requirement after hurricanes, particularly with Hurricane Maria, which damaged 472,000 homes in 2017.

“If your house is not habitable because of Maria and your loan requires it be insured while your claims for repair are pending, who’s going to insure that and help you out?” Twomey asked.

The Federal Housing Authority, which backs the loans, issued a foreclosure moratorium for hurricane victims in 2017. But that freeze expired in 2018 after two extensions. Wall Street investors and banks started filing foreclosure claims almost immediately.

María Isabel Menéndez Soto, 70, lives in a quiet neighborhood in Arecibo on Puerto Rico’s northern coast. Last year, she nearly lost her small two-story home.

Photo by Alberto Bartolomei | Center for Investigative Journalism

María Isabel Menéndez managed to keep her house after her lawyer became aware that a transaction in the process of selling the loan between financial institutions never happened.

The culprit wasn’t the flooding from Maria’s deluge or the fire that broke out inside her washer/dryer during the hurricane. It was the reverse mortgage Menéndez Soto had obtained in 2012.

She did not discover until last September, via a 10-day eviction letter, that her loan was not only in default but already had gone through a federal foreclosure proceeding and been sold at auction.

The foreclosure was triggered by an allegation that Menéndez Soto was behind on her hazard insurance. The proceedings had been frozen during the Maria foreclosure moratorium, until September 2018.

New Jersey-based Reverse Mortgage Funding and Celink, its servicer, filed for the foreclosure, saying Menéndez Soto owed about $6,500 on her insurance. Representatives from both companies failed to respond to questions about the case.

Menéndez Soto said a marshal from the courts showed up with an eviction notice, a moment she described as crippling.

“I hid in the room, closed the door and threw myself on my knees, and I said: ‘God, this is in your hands. I do not know what comes next.’”

She contacted lawyer friends who referred her to Puerto Rico Servicios Legales, which focuses on low-income help. Attorney Rafael Rodríguez Roselló untangled the situation, identifying various administrative errors and proving that Menéndez Soto had correctly paid for her insurance. He unwound the sale of her property and she says she paid $3,700 to get back on track.

Not all of Rodríguez Roselló’s clients are so lucky. In recent years, as the reverse mortgage market has consolidated to a few major players, lenders have sold off their mortgages – which can lead to a revolving, and confusing, cast of names holding borrowers’ paperwork.

Rodríguez Roselló said all of his cases involve mortgages that have been sold at least once.

“They will sell to a company in the U.S., and that’s where the problems begin: communication, language barriers, lack of documents or evidence,” he said.

Loan companies unaware of special property tax exemptions

The reverse mortgage requirement that borrowers keep current with local property taxes conflicts with special tax exemptions in Puerto Rico.

Thousands on the island do not pay taxes under agreements such as homestead tax exemptions, intended to protect homes from becoming unaffordable for low-income, senior or disabled residents.

When new servicers aren’t aware of those arrangements, the consequences can be devastating.

That’s what happened to Luis Nieves, 80, and Ada Guzmán, 75, who took out a reverse mortgage in 2009 on the home they’ve now lived in for 55 years in Carolina, on Puerto Rico’s northeast coast.

Under threat of foreclosure, they had to prove several times to their services, JB Nutter, that they were exempt from taxes.

Photo by Alberto Bartolomei | Center for Investigative Journalism

In the case of Luis Nieves and Ada Guzmán, the interests and charges accrued on the mortgage on almost exceed the value of the property.

Then, unbeknownst to Nieves and Guzmán, their insurance company stopped sending proof of their policy to the Kansas City-based firm. In 2014, JB Nutter filed for foreclosure of their house, citing lack of insurance.

The couple was able to provide proof they had a policy but unable to get receipts showing the payments as required by the company. Representatives from JB Nutter did not respond to questions for this report.

“I cried,” Luis Nieves said. “I couldn’t sleep, thinking about this, that we would have to move.”

The case stretched out for five years. The couple prepared to move out of their home and put down a $1,000 deposit on a rental property. When Hurricane Maria wrecked the rental property, and the owner kept half of their deposit, they decided to fight the foreclosure instead.

After a string of pro bono attorneys could not resolve the case, Rodgríguez Roselló, also working for free, took over in May 2019. He stopped the foreclosure.

Photo by Alberto Bartolomei | Center for Investigative Journalism

Rafael Rodríguez Roselló, a lawyer from Legal Services, represented María Isabel in her foreclosure lawsuit.

But another problem looms: The property, a modest single-story cement home, is among the 7,100 on the island with active reverse mortgage loans hit by lagging property values. The accruing interest and fees are pushing the mortgage balance close to what the couple might be able to recoup in a sale – a danger zone for reverse mortgages. The median list price in their neighborhood is about $110,000.

They are better off than many.

Records from the commonwealth’s financial regulator show that many current reverse mortgage loans on the island included the projection that home values would rise about 6% a year. Instead, they have slid by about 4%.

That gap won’t hurt borrowers in the short term. But it will have an impact when borrowers or their heirs try to pay off a loan balance to keep the home. It also will add to pressure on the Federal Housing Administration’s mortgage insurance fund, which pays lenders the difference between ballooning loan balances and actual market values after borrowers die.

With their high financing costs upfront and risks of foreclosure, reverse mortgages are not a good proposition for Puerto Rico’s seniors, said Rogelio Cardona, an accounting professor at the University of Puerto Rico, Río Piedras.

He and co-researcher Karen Castro-González advocate for less expensive alternatives like refinancing at a lower interest rate or downsizing by selling the home and moving to a smaller house or apartment.

Problems with reverse mortgages often crop up since many are sold to U.S.-based financial institutions that send warning letters in English and seek legal judgements in San Juan’s federal courthouse, “where the proceedings are in English, are more expensive and all cases are processed faster than in the local courts,” Cardona said.

“Any senior who decides to obtain a reverse mortgage must read carefully all the financing documents, or have a trusted family friend or attorney do so, and ask a lot of questions,” Cardona said.

Reverse mortgage reforms gut market in Puerto Rico

Moneyhouse acknowledges that reverse mortgages aren’t a solution for all Puerto Ricans.

Levis said his company does use bilingual U.S.-based servicers, including Reverse Mortgage Solutions in Houston. He acknowledged problems with inconsistent mail delivery but said borrowers receive second and third notices, as well as phone calls, before a default action begins.

But he criticized the federal government’s response to a surge in foreclosures for closing the door to too many seniors seeking the loans.

Gradually over the past five years, the HUD has ramped up financial requirements for seniors, lowered how much could be borrowed and added some mandatory set-asides nationwide – making the product less appealing for many.

Levis acknowledged HUD had to adjust the program to address the spike in foreclosures, including in Puerto Rico, but said the government overcorrected by ratcheting down principal limits and adding the set-aside funds.

The set-aside withholds some reverse mortgage proceeds to help cover taxes and insurance charges throughout the life of the loan, ensuring a senior won’t forget and miss an important payment that could lead to foreclosure.

“The changes they made were massive – but the issues we face in Puerto Rico are a lot different than California and a lot different than Philadelphia,” Levis said.

Differences on the island range from a lower cost of living, lower home values and cultural habits of saving money, he said.

Today, some of Puerto Rico’s seniors can borrow a maximum of $15,000 on their $100,000 home because of the new federal policies. What once might have seemed enticing is less so.

Moneyhouse used to average 50 to 60 reverse mortgage loans a month, with spikes up to 120. In the first quarter this year, the company closed just four.

This report was produced in partnership with Grand Valley State University, with financial support for the Centro de Periodismo Investigativo from the McGraw Center for Business Journalism at the Craig Newmark Graduate School of Journalism at the City University of New York and the Economic Hardship Reporting Project.

Es un abuso, una usura de la peor calaña que cometen con las personas mayores en los reverse mortage. Por error de un dólar ($1.00) en el reembolso al banco de las contribuciones de la propiedad que ellos pagaron al Crim de $3,400, para poder tener una deuda qujustifique una ejecución de hipotea. Por eso, pudieron poner la la casa de mi madre en foreclosure, y no fue por error, sabían lo que estaban haciendo. Yo misma le ayudé con ese reembolso, lo hice por teléfono hablando con un oficial de servicio con un numero de confirmación del pago que me dieron verbalmente. Pero por ese dólar, devolvieron el pago , luego de varios días (ganaron intereses de él), y nos lo devolvieron a la cuenta sin notificarlo. De inmediato, tiraton la hipoteca a foreclosure, todo esto en menos de un (1) mes. No solo eso, poci tiempo antes, le cambiaron el nombre a la compañia para verderse a sí mismos para las carteras de propiedades y subirle los topes de intereses de forma astronómica. Nuestro Reverse fue hecho a un banco local (Money House, luego fue vendido a James B.Nutter en EUA, luego a Reverse Mortgage Funding que hace poco es Celink. Si una persona mayor pierde sus capacidades y no puede dar seguimiento a estos bribones, se queda en la calle o se pierde parte del capital o equity que le corresponde al envejeciente y/o sus herederos. No pueden evolucionar la propiedad en renta total o parcial para generar ingresos adicionales, por lo que tienen que morir allí, sin que los envejevientes y sus familias puedan ayudarse con ingreso adicional para ayudar a su familiar. Esto solo algo de las muchas situaciones que hemos tenido y descubierto. Una abogada me mencionó que es posible comprar la propiedad como primer comprador durante un mes si se estan vendiendo las carteras entre instituciones. El problema de eso es tener la capacidad de pago en ese momento o de financiamiento, pero sobre todo, ENTERARSE, así que ojos bien abiertos. Es una ley y sistema de financiamiemto que tiene que cambiar o desaparecer, y ojalá que se haga una demanda de clase para luchar en contra de la explotación legalizada a los envejecientes, en este caso, no por sus familiares como tanto alegan, sino por las instituciones financieras y el ciego e ineficiente gobierno en PR y EUA que por años lo ha permitido.